The Operators

Investor

profiles

Each profile decodes the strategy, the structure, and the rare insights behind one of the great M&A fortunes. Read what they did, then steal what works.

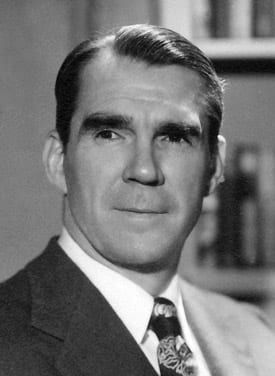

Carl Icahn

The Corporate Raider

He had no love for airlines and barely flew. When Carl Icahn set his sights on TWA, he turned a tired company into one of the most profitable trades of his career, then walked away before the wreckage.

Read playbook

Michael Milken

The Junk Bond King

He built the high-yield bond market from scratch, financed the entire raider era, became the highest-paid man in the history of American finance, and then watched it all collapse in a federal indictment.

Read playbook

Henry Kravis

The Buyout King

With his cousin George Roberts, Henry Kravis turned the leveraged buyout from a fringe Bear Stearns tactic into a global industry, and pushed the model all the way to a $31 billion deal that nearly broke his own firm.

Read playbook

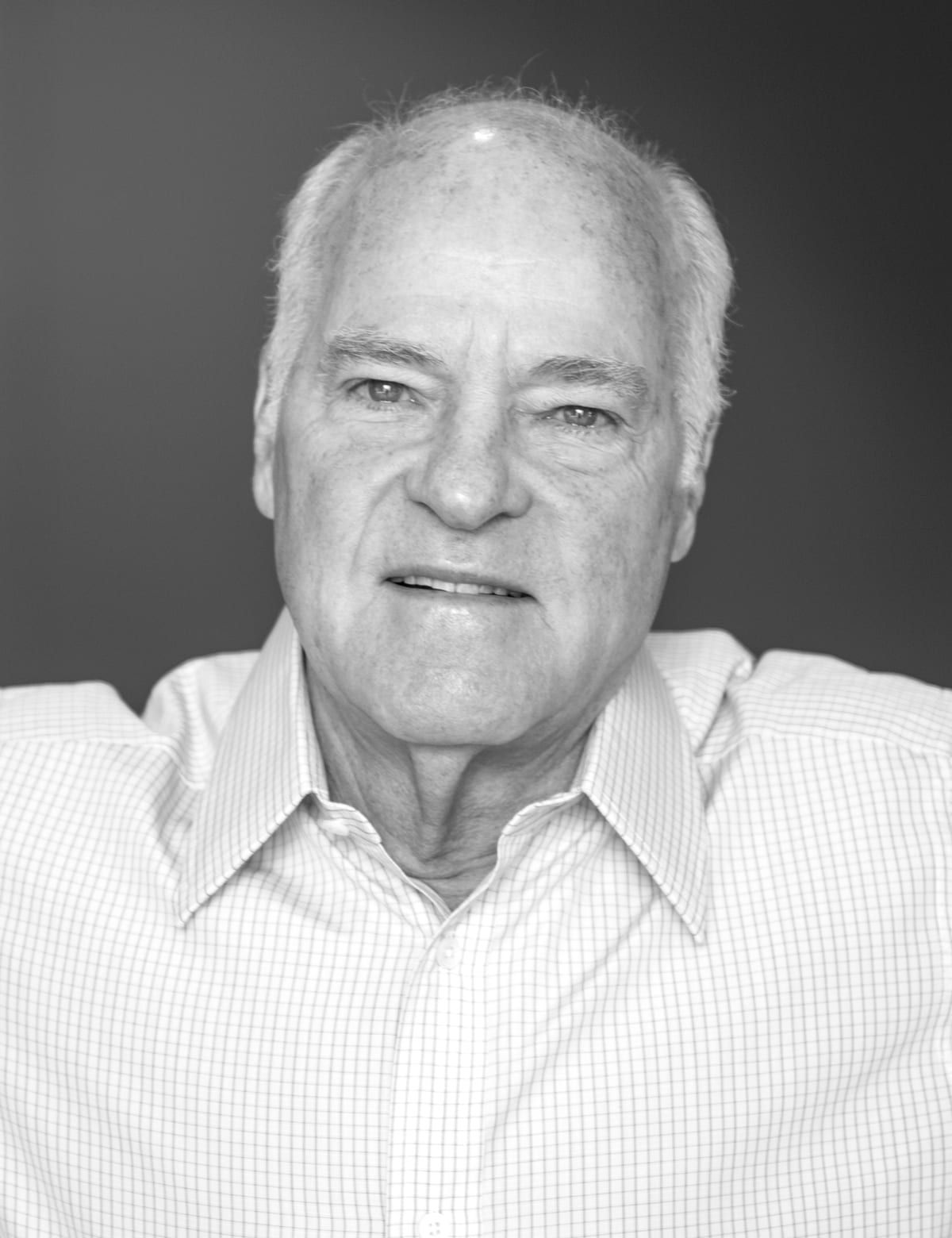

T. Boone Pickens

The Oilman Raider

A West Texas wildcatter who decided the cheapest oil in America was not in the ground at all. It was trading on the New York Stock Exchange, locked inside the complacent oil majors, and he could get at it with a phone and a printer.

Read playbook

Ivan Boesky

The Arbitrageur

He turned merger arbitrage into a high art, became the most quoted Wall Street figure of the mid-1980s, and then ruined the profession for everyone by paying for the one thing arbitrage was never supposed to need: the answer in advance.

Read playbook

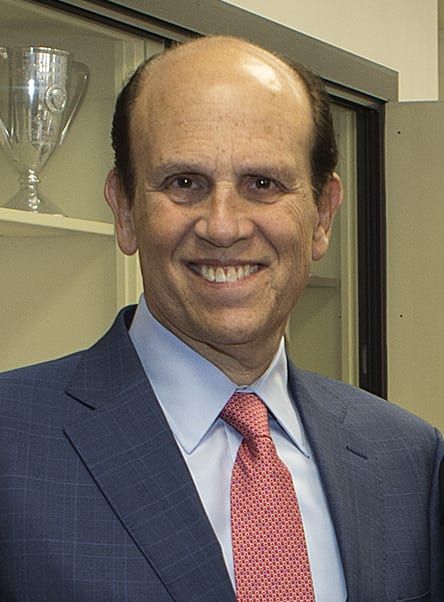

Ronald Perelman

The Leveraged Acquirer

He took a small jewelry-and-licorice company called MacAndrews & Forbes and turned it into a borrowing platform, then used it to seize Revlon and rewrite American takeover law in the process.

Read playbook

Wayne Huizenga

The Rollup King

He built three Fortune 500 companies from scratch with the same playbook: pick a fragmented, sticky-revenue industry, buy the smallest operators on the cheap, integrate aggressively, and exit at a multiple no single operator could ever command alone.

Read playbook

Brad Jacobs

The Modern Rollup Architect

He has built five publicly traded billion-dollar companies, each through serial acquisitions, in five separate industries. The playbook he uses is the most widely studied operator manual in modern private equity, and in 2024 he wrote it down.

Read playbook

Daniel K. Ludwig

The Invisible Billionaire

He was the first American billionaire on the Forbes list, the richest man in the country for most of the 1970s, and almost nobody recognised him on the street. He built one of the largest private industrial empires in history by vertically integrating every commodity he touched and never granting an interview.

Read playbook

Mark Leonard

The Ghost Compounder

He has built one of the great compounders of the 21st century out of more than 900 acquisitions of tiny vertical-market software companies. He has held a single in-person shareholder Q&A in three decades. There are almost no public photographs of him. The playbook he writes down each year in his shareholder letters is the most carefully studied document in modern software M&A.

Read playbook

John C. Malone

The Cable Cowboy

He built the modern American cable industry through 482 acquisitions and a financial structure so sophisticated that Warren Buffett once said he would not own a Malone company because he could not understand the balance sheet. Forty years later, Malone is still the largest individual landowner in the United States and the architect of more tax-efficient structures than any other operator alive.

Read playbook

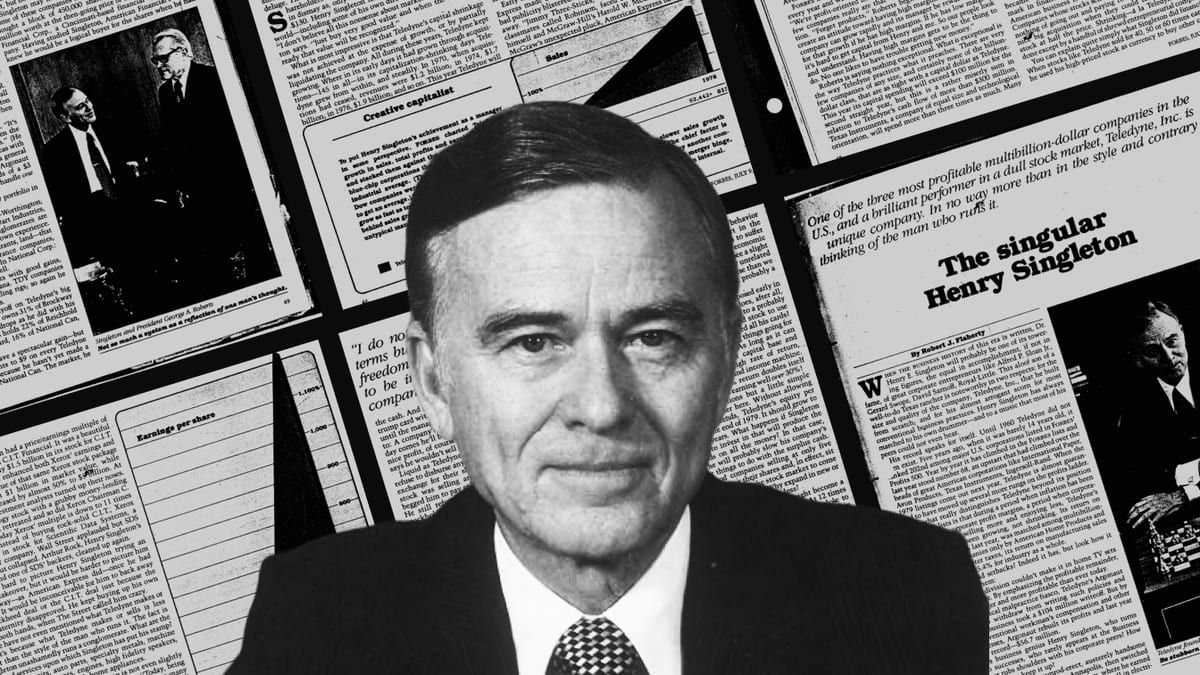

Henry Singleton

The Capital Allocator

He built Teledyne through 130 acquisitions in the 1960s when his stock was overvalued, then stopped acquiring and bought back almost 90 percent of his own shares when his stock was cheap. The total shareholder return was 20-fold over 24 years. Warren Buffett called him the best operator in American business. He almost never gave an interview.

Read playbook

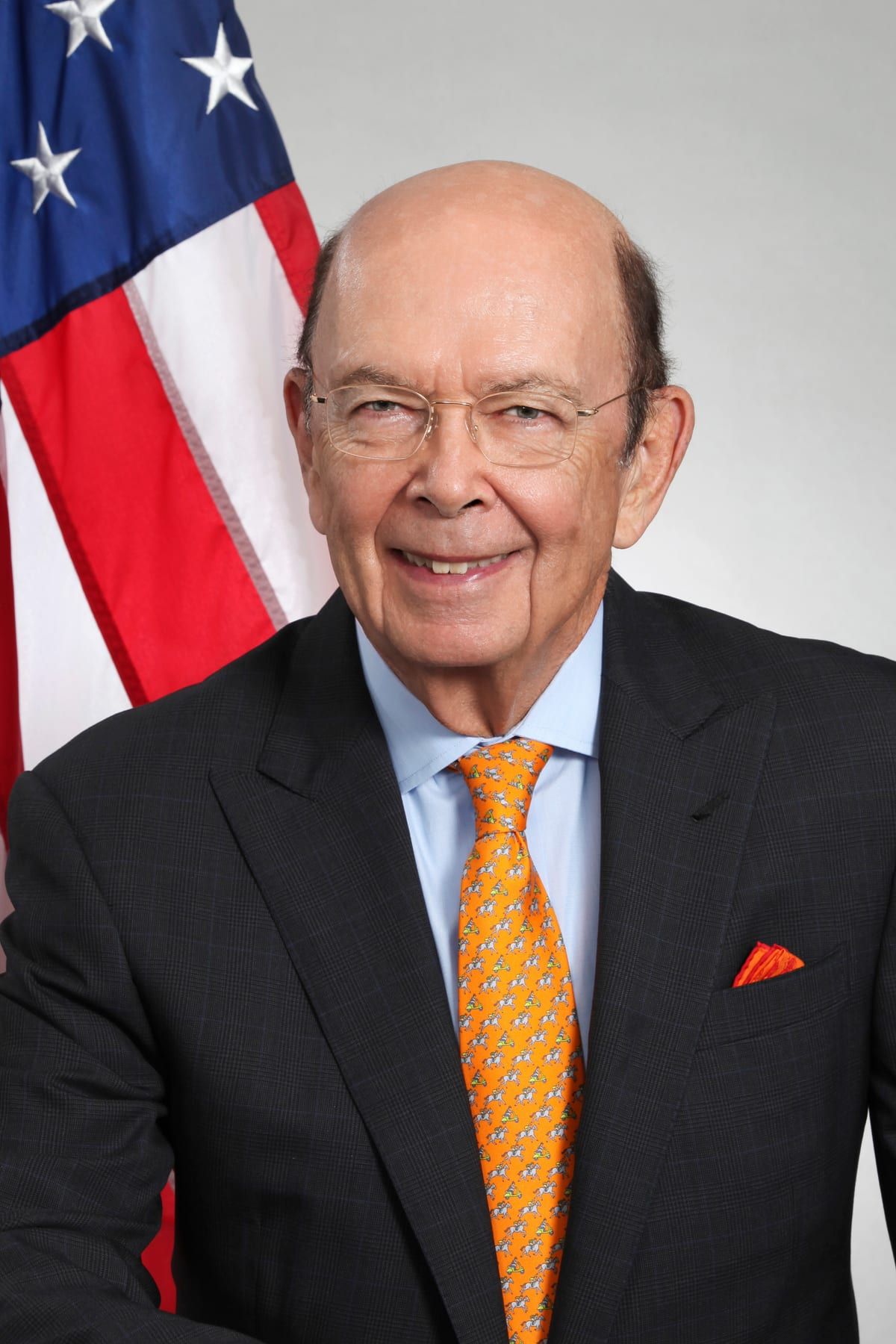

Wilbur Ross

The Distressed Specialist

He spent 24 years running Rothschild's bankruptcy desk before deciding he could do the trade better on his own. He bought eight bankrupt steel mills for $1.5 billion, fixed them, and sold the combined company to Mittal four years later for $4.5 billion. The same playbook ran through coal, textiles, and auto parts.

Read playbook

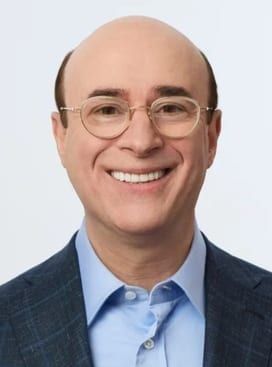

Thomas H. Lee

The Consumer-Brand LBO Craftsman

He bought Snapple in 1992 for $135 million, took it public eight months later, and sold it to Quaker Oats in 1994 for $1.7 billion. The Snapple trade is the most-studied single LBO in private-equity history because it ran the entire playbook in twenty-four months.

Read playbook