The Finance Playbook

College Doesn’t

Teach You.

Written by active bulge-bracket bankers. Get the Dealmaker’s Playbook free today: six legendary moves from the titans of finance and the lesson to steal from each. Then one deal, banker, or concept decoded every Sunday.

Free instant download

Get the Dealmaker’s Playbook.

Six legendary plays from Pickens, KKR, Perelman, Milken and Ludwig, with the lesson to steal from each. Sent straight to your inbox.

Takes 10 seconds. No spam, no credit card, unsubscribe in one click. Then The Sunday Brief lands every Sunday at 8:00 AM ET.

- Read by Wall Street professionals

- 5-minute Sunday read

- Free forever

-

Decode the landmark deals

One landmark transaction every Sunday, broken into the structure, the financing, and the actual banker terminology used on the deal. Fluency you won’t get from any textbook.

-

Master the technicals

Valuation frameworks, NWC mechanics, and quality-of-earnings drills as they are actually run on the desk by analysts working the live deals.

-

Steal the career edges

The unspoken rules of bulge-bracket, boutique and PE seats, written by insiders currently working at the top desks on Wall Street.

The Operators

Learn from the operators who built empires

Each profile decodes the strategy, the structure, and the rare insights behind one of the great M&A fortunes. Copy what works, leave the rest.

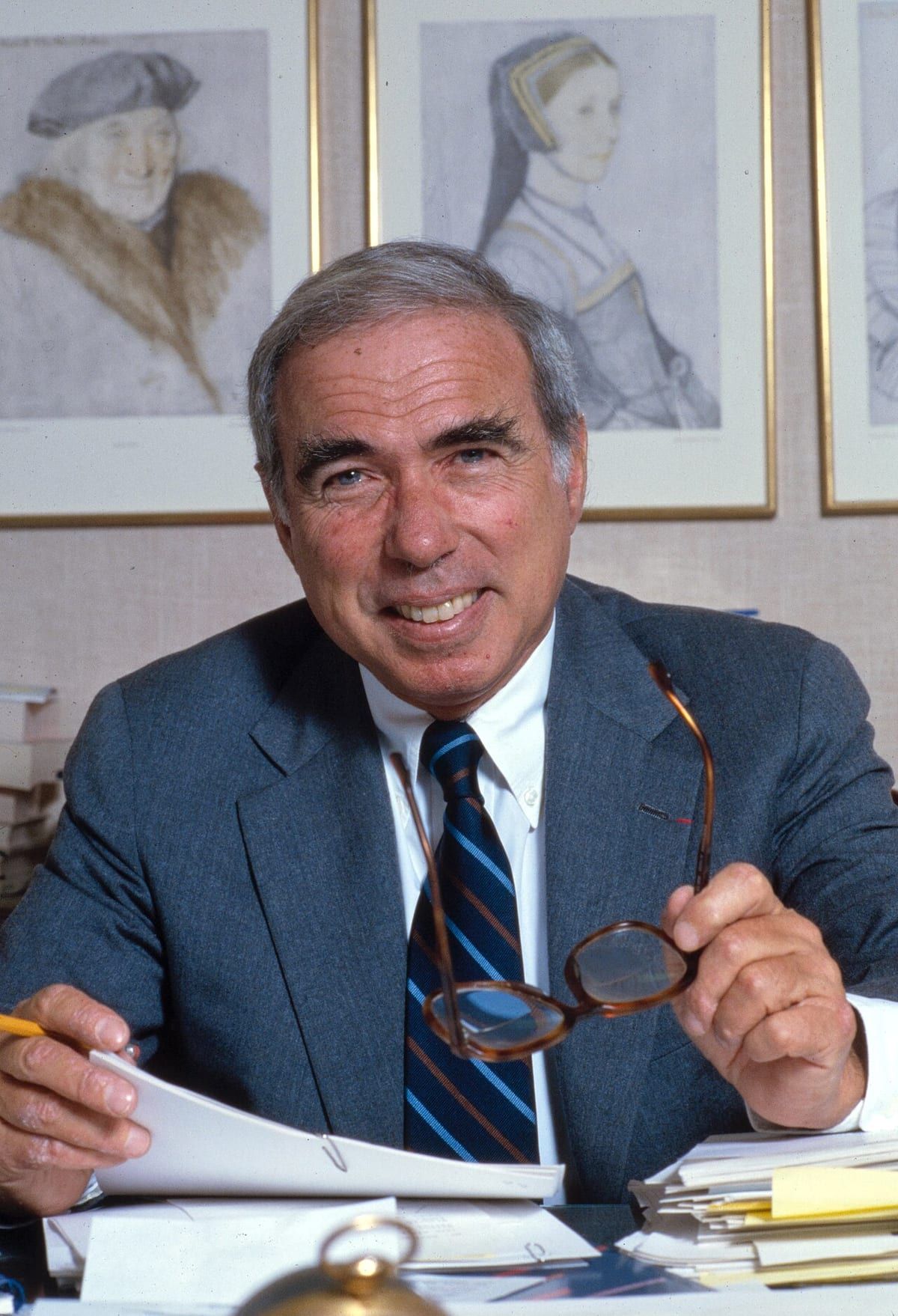

Carl Icahn

The Corporate Raider

He had no love for airlines and barely flew. When Carl Icahn set his sights on TWA, he turned a tired company into one of the most profitable trades of his career, then walked away before the wreckage.

Read playbook

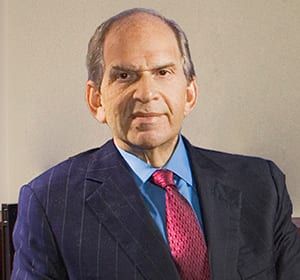

Michael Milken

The Junk Bond King

He built the high-yield bond market from scratch, financed the entire raider era, became the highest-paid man in the history of American finance, and then watched it all collapse in a federal indictment.

Read playbook

Henry Kravis

The Buyout King

With his cousin George Roberts, Henry Kravis turned the leveraged buyout from a fringe Bear Stearns tactic into a global industry, and pushed the model all the way to a $31 billion deal that nearly broke his own firm.

Read playbook

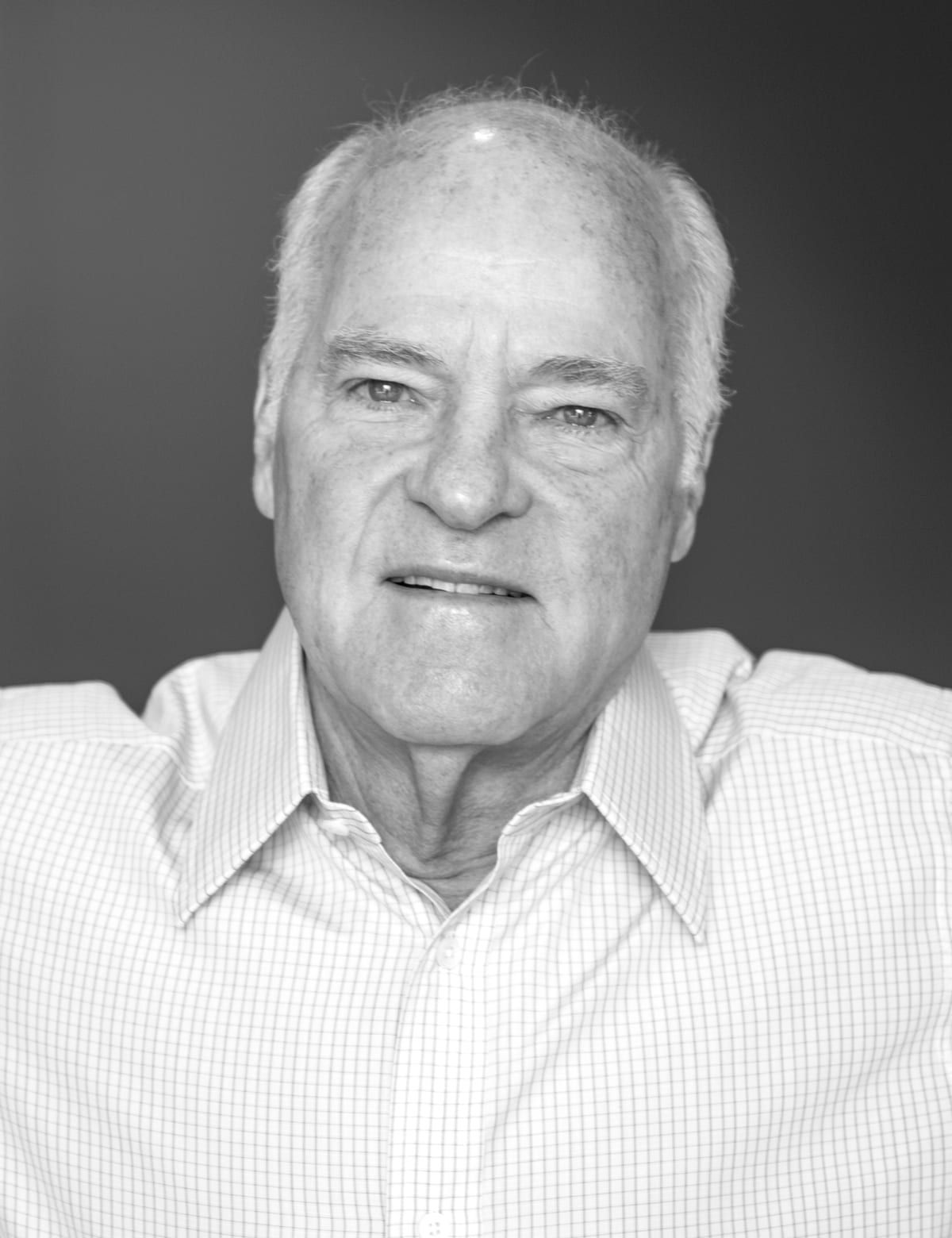

T. Boone Pickens

The Oilman Raider

A West Texas wildcatter who decided the cheapest oil in America was not in the ground at all. It was trading on the New York Stock Exchange, locked inside the complacent oil majors, and he could get at it with a phone and a printer.

Read playbook

Ivan Boesky

The Arbitrageur

He turned merger arbitrage into a high art, became the most quoted Wall Street figure of the mid-1980s, and then ruined the profession for everyone by paying for the one thing arbitrage was never supposed to need: the answer in advance.

Read playbook

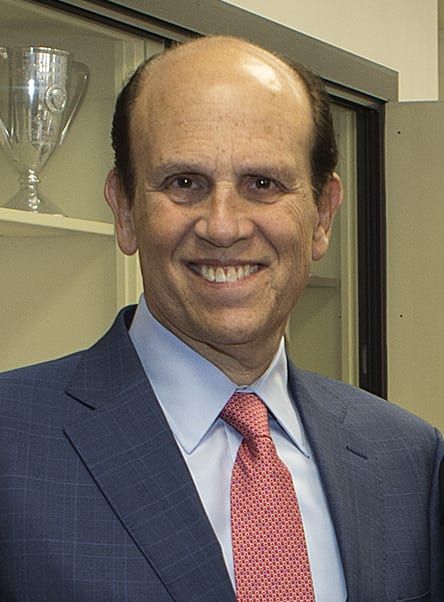

Ronald Perelman

The Leveraged Acquirer

He took a small jewelry-and-licorice company called MacAndrews & Forbes and turned it into a borrowing platform, then used it to seize Revlon and rewrite American takeover law in the process.

Read playbookThe Bankers

And from the bankers who advised them

Five careers that built modern mergers advisory. Felix Rohatyn, Bruce Wasserstein, Joe Perella, Bob Greenhill and Jimmy Lee. Every analyst and associate working in M&A today is executing on a playbook one of these five men wrote.

Felix Rohatyn

The Dealmaker Statesman

He turned Lazard Freres into the most influential mergers boutique on Wall Street, advised on the giant conglomerate deals of the 1960s and 1970s, and personally rescued New York City from bankruptcy in 1975. Felix Rohatyn is the model for the modern M&A adviser: small team, no balance sheet, immense influence.

Read playbook

Bruce Wasserstein

Bid 'Em Up Bruce

He invented the modern hostile-takeover playbook at First Boston, taught it to a generation of M&A bankers, then walked across the street to found Wasserstein Perella and prove it was portable. By the time he died in 2009 he had advised on more than a thousand deals worth a trillion dollars.

Read playbook

Joseph Perella

The Franchise Builder

He has founded the M&A practice at one major firm and three independent boutiques. Joe Perella did not invent the modern advisory model, but he built more of its modern institutions than any other living banker. First Boston M&A, Wasserstein Perella, Morgan Stanley M&A, and finally Perella Weinberg Partners.

Read playbook

Robert Greenhill

The First Modern M&A Banker

He built the M&A department at Morgan Stanley in 1972, four years before First Boston or Goldman had one of their own. Bob Greenhill is the godfather of dedicated mergers advisory on Wall Street and the founder of one of the most respected boutiques of the modern era.

Read playbook

James B. Lee Jr.

The King of Leveraged Finance

He invented the modern syndicated leveraged loan, financed almost every major LBO of the 1990s and 2000s, and turned Chase (later JPMorgan) into the dominant debt house on Wall Street. Jimmy Lee did not advise on deals; he made them possible by writing the cheque before anyone else would.

Read playbookFree tools

Learn by doing

The LBO Calculator

Drag the leverage, growth, and exit sliders and watch MOIC and IRR respond live. The arithmetic behind every buyout since KKR.

Open the calculator → Interactive modelMerger Math: Accretion / Dilution

Set the price, the funding mix, and the synergies, and watch what the deal does to EPS. The first question every board asks.

Run the merger math → Interactive modelThe DCF Calculator

Value a company from its cash flows, with a live sensitivity grid that shows what the discount rate really does.

Value a company → ReferenceThe M&A Glossary

Every deal term from poison pill to MOIC, defined in plain English and linked to the deals where it happened.

Browse the glossary → Free downloadThe Dealmaker’s Playbook

Six legendary moves from the titans of finance and the lesson to steal from each. Free, straight to your inbox.

Get the free guide →Playbooks and primers

Deal studies, rollup tactics, and plain-English explainers. Filter by what you want to learn next.

Continuation Funds and GP-Led Secondaries: How PE Firms Hold Their Best Deals Longer

Continuation funds are the fastest-growing exit route in private equity. They let a GP sell a portfolio company from one of its own funds to a new fund it also manages, with fresh outside capital. Here is how the structure works, why LPs accept it, and what every PE analyst should understand about the mechanics.

Read primerRollover Equity in M&A: How Sellers Stay Invested in Their Own Deal

Rollover equity is the portion of a sale price that the founder, management team, or existing investors keep in the new company rather than taking in cash. In private-equity-backed acquisitions, rollover equity is the single most important alignment mechanism between the buyer and the people who will keep running the business. Here is exactly how it works and what an analyst needs to model.

Read primerNAV Financing in Private Equity: How GPs Borrow Against Their Whole Portfolio

NAV financing, also called fund-level financing or NAV lending, is the fastest-growing form of leverage in private equity. A GP pledges the value of an entire portfolio of companies as collateral for a loan to the fund, then uses the proceeds for distributions, follow-on investments, or to support struggling assets. The structure has roughly tripled since 2020 and is now one of the most controversial topics between GPs and LPs.

Read primerWilbur Ross

He spent 24 years running Rothschild's bankruptcy desk before deciding he could do the trade better on his own. He bought eight bankrupt steel mills for $1.5 billion, fixed them, and sold the combined company to Mittal four years later for $4.5 billion. The same playbook ran through coal, textiles, and auto parts.

Read profileThomas H. Lee

He bought Snapple in 1992 for $135 million, took it public eight months later, and sold it to Quaker Oats in 1994 for $1.7 billion. The Snapple trade is the most-studied single LBO in private-equity history because it ran the entire playbook in twenty-four months.

Read profileNet Working Capital in M&A

The single most contested adjustment in any acquisition agreement. Net working capital is where buyers claw back the last 1 to 3 percent of purchase price after closing. Every analyst should understand it before the model is built.

Read primerThe M&A Deal Lifecycle

From the first banker pitch to the post-closing integration. The eight stages of every modern M&A transaction, what each one is actually for, and where the value is won or lost.

Read primerWayne Huizenga

He built three Fortune 500 companies from scratch with the same playbook: pick a fragmented, sticky-revenue industry, buy the smallest operators on the cheap, integrate aggressively, and exit at a multiple no single operator could ever command alone.

Read profileBrad Jacobs

He has built five publicly traded billion-dollar companies, each through serial acquisitions, in five separate industries. The playbook he uses is the most widely studied operator manual in modern private equity, and in 2024 he wrote it down.

Read profileMark Leonard

He has built one of the great compounders of the 21st century out of more than 900 acquisitions of tiny vertical-market software companies. He has held a single in-person shareholder Q&A in three decades. There are almost no public photographs of him. The playbook he writes down each year in his shareholder letters is the most carefully studied document in modern software M&A.

Read profileJohn C. Malone

He built the modern American cable industry through 482 acquisitions and a financial structure so sophisticated that Warren Buffett once said he would not own a Malone company because he could not understand the balance sheet. Forty years later, Malone is still the largest individual landowner in the United States and the architect of more tax-efficient structures than any other operator alive.

Read profileHenry Singleton

He built Teledyne through 130 acquisitions in the 1960s when his stock was overvalued, then stopped acquiring and bought back almost 90 percent of his own shares when his stock was cheap. The total shareholder return was 20-fold over 24 years. Warren Buffett called him the best operator in American business. He almost never gave an interview.

Read profileThe Rollup Playbook: How Private Equity Builds Empires by Buying Small

A rollup buys dozens of small companies in the same industry, merges them, and sells the combined business at a much higher multiple. The arithmetic is one of the most reliable ways to build serious wealth in modern private equity.

Read primerThe Search Fund Model: How a $400,000 Bet Can Become a $50 Million Exit

A search fund is the most accessible path in finance to running and owning a real company. The model takes about $400,000 of search capital, two years of work, and produces returns that the Stanford GSB has tracked at roughly 35 percent IRR over four decades.

Read primerWhat Is a Leveraged Buyout?

The nuclear weapon of 1980s finance, explained in plain English. Before you can understand the deals, you need to understand the weapon.

Read primerThe Night They Carved Up RJR Nabisco

A $25 billion wager that would end careers, forge fortunes, and change Wall Street forever, the inside story of the largest leveraged buyout in history.

Read storyHenry Kravis

With his cousin George Roberts, Henry Kravis turned the leveraged buyout from a fringe Bear Stearns tactic into a global industry, and pushed the model all the way to a $31 billion deal that nearly broke his own firm.

Read profileMichael Milken

He built the high-yield bond market from scratch, financed the entire raider era, became the highest-paid man in the history of American finance, and then watched it all collapse in a federal indictment.

Read profileCarl Icahn

He had no love for airlines and barely flew. When Carl Icahn set his sights on TWA, he turned a tired company into one of the most profitable trades of his career, then walked away before the wreckage.

Read profileDaniel K. Ludwig

He was the first American billionaire on the Forbes list, the richest man in the country for most of the 1970s, and almost nobody recognised him on the street. He built one of the largest private industrial empires in history by vertically integrating every commodity he touched and never granting an interview.

Read profileMultiple Arbitrage Explained: Why Private Equity Pays More Than the Math Suggests

A small company doing $1 million in EBITDA sells for four times earnings. A mid-sized company doing $20 million in EBITDA sells for nine times. The spread is structural, durable, and the single most important reason private equity returns work.

Read primerHow to Spot an LBO Target: A Practical Checklist

Private equity buys roughly 8,000 American companies a year. The ones that produce the best returns share a small list of features any investor can screen for. Here is the checklist that has worked for forty years.

Read primerPoison Pills, Explained

The corporate defense that made hostile takeovers ten times harder, how the shareholder rights plan works, and why it changed the balance of power in the boardroom.

Read primerThe Predators' Ball

Every spring, the most feared men in American finance flew to Beverly Hills to trade favors and financing with Michael Milken. It looked like a conference. It was a marketplace.

Read storyT. Boone Pickens vs Gulf Oil

The raid that proved no oil major was safe, and that you could lose the company, win the trade, and reshape an entire industry in the process.

Read storyRon Perelman Takes Revlon

A beauty company, a leveraged outsider, and a Delaware court ruling that changed the rules of every hostile takeover that followed.

Read storyKKR and the Beatrice Buyout

The $6.2 billion deal that proved the leveraged buyout could scale into the billions, and set the stage, two years later, for RJR.

Read storyRonald Perelman

He took a small jewelry-and-licorice company called MacAndrews & Forbes and turned it into a borrowing platform, then used it to seize Revlon and rewrite American takeover law in the process.

Read profileIvan Boesky

He turned merger arbitrage into a high art, became the most quoted Wall Street figure of the mid-1980s, and then ruined the profession for everyone by paying for the one thing arbitrage was never supposed to need: the answer in advance.

Read profileT. Boone Pickens

A West Texas wildcatter who decided the cheapest oil in America was not in the ground at all. It was trading on the New York Stock Exchange, locked inside the complacent oil majors, and he could get at it with a phone and a printer.

Read profileNothing in this category yet. More is on the way.